Did you know that offering your customers convenient payment processing improves sales, boosts customer retention and promotes brand loyalty?

Customers are more likely to complete purchases when businesses offer different payment options, such as credit cards and digital wallets (Apple Pay or Google Pay), than when they offer one option. Accepting different payment methods, if optimized well, can give your business a competitive edge.

Before you start accepting card payments, it’s important to familiarize yourself with the technical terms associated with payment processing.

Understanding the technical jargon will help you:

- Learn about the tools and services you need to accept payments

- Make an informed decision about a partner that can make payment processing easier

- Learn about the industry standards and regulations you need to comply with

To help you navigate the world of payment processing, we’ve compiled a terminology guide that includes in-depth definitions of the basics you need to learn.

We’ve organized all terms into related subtopics and included detailed explanations and examples on the role each of these basics play in payment processing.

These definitions will make payment processing easier to understand.

Credit Card Processing Fees

1. Monthly Fee

Definition of Monthly Fee

A regular charge made monthly to a merchant processor to cover the costs of maintaining the processor’s infrastructure.

Think of it as a service fee that covers the upkeep of the merchant processor’s system to ensure transactions are processed smoothly.

The fee also covers any additional services provided, such as monthly statements.

There are four common types of monthly fees, including:

- Maintenance fee: Covers the operational costs of keeping the merchant’s account active and providing customer support

- Statement fees: A charge for providing a detailed monthly statement of a merchant’s payment activity

- PCI compliance fee: The costs of adhering to the Payment Card Industry (PCI) standards

- Gateway fee: Cost of providing and maintaining a payment gateway

Some payment processors offer these fees as a bundled package with a flat rate, while others charge each fee individually.

Related Terms:

- Transaction Fee

- Setup Fee

2. Setup Fee for Payment Processing

Definition of Setup Fee

A one-time fee is charged by a payment processing company to configure a merchant account and enable a business to accept electronic payments.

Image Credit: https://unsplash.com/photos/q3o_8MteFM0

Alt: woman swipes card at a point-of-sale terminal

Things a Setup fee goes towards:

- Opening a merchant account

- Setting up the necessary software or hardware for payment processing such as a point-of-sale (POS) system or a virtual terminal

- Payment gateway integration

- Providing training and support to the business

The fees are charged as a flat rate and depend on factors, such as the type of business or the payment processing system a store needs.

For instance, setup fees for a traditional brick-and-mortar store that requires a POS system will differ from those of an online store that needs a payment gateway.

Setup fees are non-refundable, but they can be negotiated with your payment processor.

The fees are usually added to the total processing costs but are not included in the monthly processing costs charged by merchant processors.

Synonyms: Startup costs, setup charges

3. Interchange Fees

Interchange rates are the fees passed through by banks (who are first charged by Visa, MasterCard, American Express or other Card Network Associations for processing credit or debit card payments. These cover the risk of approving the purchase, fraud, and handling essential overhead business costs.

Interchange fees are set by each card network and are reviewed twice a year, once in April and once in October. Payment Processors add a few basis points to the Interchange rates so they can make money. The fees are charged as a percentage of the transaction and are present in every transaction.

Supermarkets have extremely low interchange rates as a business category because they have a massive and consistent volume of handheld swipe, low-risk transactions that are relatively low in dollar amount per charge. There is not a lot of fraud out of grocery stores. An example of the Visa interchange fee for a swiped credit card at a supermarket is 1.15%, which means that a $100 purchase will incur a $1.15 interchange fee. But the processor will add ten basis points to that rate for their margin so the supermarket will now be charged 1.25% and in turn for a $100 purchase will incur a $1.25 interchange fee.

The interchange rates vary and depend on factors, such as:

- Type of card used: Debit cards have lower interchange fees than credit cards since the customer spends his or her own money as opposed to credit cards, where the customer is borrowing the money.

- Service paid for: Interchange fees are expensive for high-risk merchants who receive a lot of chargebacks and returns. One such example is a furniture store where customers often regret expensive purchases and return items, initiating a chargeback or refund process.

- Type of transaction: Card-not-present transactions (virtual, ecommerce or phone purchases) have higher interchange fees since they run a higher fraud risk than card-present transactions.

The transaction fee is the charge paid over and above the interchange fees. The fee charges are typically paid in the same way as interchange. The card network has a rate charged to the merchant processor and the merchant processor add a small amount on top of it to charge the supermarket.

4. Transaction Fee for Payment Processing

Definition of Transaction Fee

A charge that businesses must pay each time they receive payment or issue a refund via a credit or debit card.

The charge ranges between $0.10 to $0.30 of every transaction processed be it a purchase or a refund chargeback, depending on the payment processor.

Transaction fees are integral in payment processing as they compensate the parties involved in making the transaction a success.

When a customer makes an online purchase using a credit or debit card, the transaction is processed through a payment gateway and sent to the merchant processor.

From here, the transaction goes through the card network, the issuing bank, the acquiring bank, and then back to the merchant processor.

Each of these entities incurs expenses for smooth and secure payment processing, and it’s these fees that the transaction fee covers.

However, while shopping for a payment processor, it’s common to see the transaction fees expressed like this 2.90% + $0.30. The fee expressed as a percentage is the interchange fee, while the one expressed as a flat rate is the transaction fee.

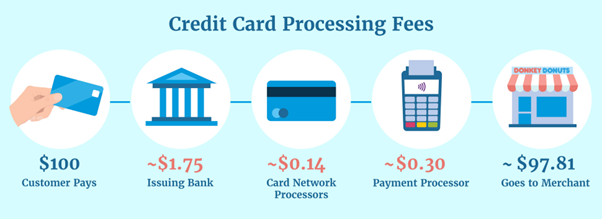

Back to the Visa supermarket charge example. The card network associations charge a transaction fee of $0.15. For every $100 payment swiped or tapped, the payment processor is charged $1.15 (interchange fee) and $0.15 (transaction fee) by Visa. The payment processor then adds their fee in to both interchange and the transaction fee. The Supermarket will now be charged: $1.25% interchange fee and $0.25 for each transaction.

5. Issuing Banks

An Issuing Bank is a financial institution that is licensed by a Card Network Association to use their brand (Visa or MasterCard etc) for their bank’s credit card and debit card program. Issuing Banks often times have dozens if not hundreds of different types of credit card and debit card programs with the Card Network Associations.

A few made-up examples of different card programs for the purpose of explanation in this article would be:

Chase Bank Family Friendly Credit Card – The Credit Card that gives you points when you buy gifts for your family.

Wells Fargo Soccer Sweepstakes Credit Card – This Credit Card gives you triple points when you use it at a soccer stadium.

The way Issuing Banks make money from these credit card programs licensed by the card network associations is that they get the percentage point split between the interchange rate and transaction fee with the card network association.

A side note: For all of the cashback points or incentive award points offered by these cards, the supermarket in this example (or the business that is selling the product or service) is losing profit for those percentage points you as the consumer get as a benefit of using your card. Those award points are added to the interchange percentage and that is why some rates are higher than others.

Image source: https://www.creditdonkey.com/credit-card-processing-fees.html

Card network transaction fees aren’t as high as interchange fees, but they still take a small portion of your sales.

The table below outlines the average interchange and transaction fees charged by four major credit card networks in the United States.

| Card Network | Interchange Fees | Transaction Fees |

| American Express | 1.35% to 3.0% | $0.10 |

| Mastercard | 1.25% to 3.15% | $0.05–$0.10 |

| Discover | 1.45% to 3.05% | $0.05–$0.10 |

| Visa | 1.15% to 3.15% | $0.05–$0.10 |

The interchange rate and transaction fee vary depending on the payment processing company. It’s, therefore, crucial to scrutinize these fees and choose a provider that offers the most transparent and fair pricing.

Also, you should know you can negotiate merchant processing fees, especially if your business handles a large volume of transactions. A discount rate as small as $0.1 per transaction can save your business $1,000 if you process 10,000 transactions.

Transaction Fees Pricing Models

Payment processing companies sell their services in the following pricing models:

Expert Tip: Setting a card minimum purchase can help lower your transaction fees since small tickets incur higher transaction fees than large tickets.

For example, a $5 ticket will accrue $0.445 per transaction, which is 8.9 percent of the transaction. In contrast, a $1,000 purchase incurs 2.9 percent of the transaction.

Interchange plus

- Interchange fees: 2.50%

- Card network fees: 0.14% + $0.05

- Payment processor’s markup: 0.15% + $0.07

- Total transaction fee = 2.93% of the transaction

Tiered Plans

The processor groups different interchange prices into a single tier and then charges a fixed price for each tier. Tiers are grouped according to the level of risk associated with the interchange fees.

6. Fraud Prevention for Payment Processing

Notably, most processors group the interchange rates into three categories: qualified, mid-qualified, and non-qualified. For instance, card present transactions swiped or read by a point-of-sale (POS) terminal are grouped together into a category with qualified rates.

The table below compares the advantages and disadvantages of these three pricing models.

| Pricing Model | Advantages | Disadvantages |

| Flat rate plans | ● Simple monthly statements

● Merchants know their exact transaction costs ● Easiest model to understand |

● Some processors may add hidden fees to the charges |

| Interchange plus | ● Most transparent pricing model

● No hidden fees |

● Hard to follow monthly statements |

| Tiered plans | ● Low transaction costs for qualified rates | ● Conceals the processing costs

● Confusing monthly statements ● Understanding the classification of a transaction is difficult |

“I have processed over $80 million in electronic payments with Total Apps. They’ve given me the best pricing and incomparable service.” – , Director of Finance, Funding Avenue

Synonyms: Transaction costs, processing costs, per-transaction fee

Related Terms:

Data Security

1. Fraud Prevention for Payment Processing

Definition of Fraud Prevention

The use of various strategies or interventions to stop nefarious financial activity. The strategies aim at protecting businesses and customers from monetary damage by safeguarding sensitive information and reducing chargebacks.

Fraud prevention involves monitoring eCommerce web stores and payment processing systems for suspicious activity, identifying potential fraud cases, and responding to fraud alerts.

It also involves the prevention measures undertaken to protect cardholder data or log-in information from being viewed by fraudsters.

Some fraud prevention techniques include the implementation of measures, such as:

- Two-factor authentication

- Encryption

- Transport Layer Security (TLS) certification

- Tokenization

To understand how these measures work, let’s first discuss some common types of fraud in payment processing.

- Data breaches: Confidential information is revealed to an unauthorized person without the knowledge of the system’s owner

- Payment fraud: Someone attempts to use a stolen credit card (or illegally obtained cardholder data) to make a transaction

- Account takeover: Cyber criminals hack into existing customers’ accounts and use the stored billing information to make purchases or resell the account.

- Employee fraud: Employees steal payment information stored on the merchant’s website or files and attempt to use the payment data on other online stores.

- Friendly fraud: Someone uses their own card to purchase something and claims they didn’t receive it or they received a damaged item. They request a refund or chargeback. The business loses the product value, they are charged for all of the transactions and they incur additional fees for chargebacks and other things.

Fraud Prevention Techniques That Deter Fraud

The following are some fraud prevention techniques that help deter fraud.

The PCI DSS includes requirements that prevent fraudsters from hacking merchants’ websites and payment servers.

Security protocols, such as encryption and firewall configuration, ensure fraudsters won’t gain access to your system and thus obtain sensitive payment information passed over public networks.

This protects merchants from employee fraud, data breaches, and account takeovers.

Tokenization

Tokenization replaces sensitive data with randomly generated characters that can’t be traced back to the original information. This safeguards cardholder data even in the event of data breaches.

Two-factor authentication

With two-factor authentication (2FA), customers are identified using two separate, distinct methods before they can gain access to something.

For instance, a customer logging in to their online account may be required to enter their password first. If the password is correct, they must then enter a one-time code sent to their email address or phone number.

2FA improves the security of customers’ accounts, which prevents account takeover and payment fraud.

Machine Learning

Machine learning uses artificial intelligence and data analytics to detect behavioral anomalies that suggest fraudulent activity. For example, large purchases made using a credit card from the same location can point to payment fraud.

With machine learning, such transactions are flagged and reviewed to confirm their authenticity.

Certain rules, such as the user ban of known fraudsters, can also be implemented with machine learning to prevent fraud.

Is Fraud Prevention Different From Fraud Detection?

Yes, fraud prevention and fraud detection are two different, yet closely related, practices that merchants use to protect themselves from financial damage.

Fraud prevention refers to the measures taken before a fraud, while fraud detection refers to the measures implemented in real time when a fraudulent transaction is taking place.

The purpose of fraud prevention is to prevent and discourage fraud, while fraud detection aims to recognize and resolve a fraudulent transaction.

For instance, tokenization is a fraud prevention measure that ensures cybercriminals don’t access payment data. Address Verification Service (AVS), on the other hand, is a fraud detection tool that prevents fraudulent transactions from going through.

The table below shows which of the two strategies (fraud prevention and fraud detection) is best suited to protect your business from four common types of fraud.

| Fraud | Fraud Prevention | Fraud Detection |

| Payment fraud | ✓ | |

| Data breaches | ✓ | |

| Employee fraud | ✓ | |

| Account takeover | ✓ |

Related Terms:

- Fraud scrubbing

- PCI compliance

- Tokenization

2. Fraud Scrubbing

Definition of Fraud Scrubbing

A process used by payment processors to detect and block fraudulent transactions or accept legitimate transactions that may appear suspicious.

The process involves running a series of checks to scrutinize a transaction, hence the word scrubbing.

Fraud scrubbing helps reduce payment fraud, which is especially prevalent in card-not-present (CNP) transactions.

Some credit card fraud schemes that can be prevented through fraud scrubbing include:

- Identity theft: A buyer uses another person’s private information to make a purchase

- Credit card theft: A customer attempts to use a stolen credit card to make online purchases

- Card testing fraud: Criminals make small purchases on stolen credit cards to find out if they have funds

- Bank Identification Numbers (BIN) attacks: Fraudsters attempt to make purchases using fake credit card numbers hoping to match legitimate ones

The following are four fraud-scrubbing techniques used to authenticate CNP transactions:

- Address Verification Service (AVS)

- Card Verification Value (CVV)

- IP address checks

- Machine learning

Here’s how each of these tools works.

Address Verification Service (AVS)

This tool verifies the ownership of a card by checking that the billing information submitted during payment processing matches the address on file at the issuing bank.

If the addresses match, an AVS response code is sent, and the transaction is authorized. If there is a mismatch in the address, the payment remains pending on the credit card account until further checks are conducted to determine its legitimacy.

The four major credit card brands in the United States (Visa, American Express, Mastercard, and Discover) support AVS. Each of the card brands has unique AVS response codes that help determine why a transaction is declined.

The following table outlines four AVS response codes that are common across all the brands.

| AVS Response Code | Meaning |

| W | Full ZIP match, no match on street address |

| X | Full street address and ZIP match |

| Y | Full street address match and partial ZIP match |

| Z | Partial ZIP match, no match on street address |

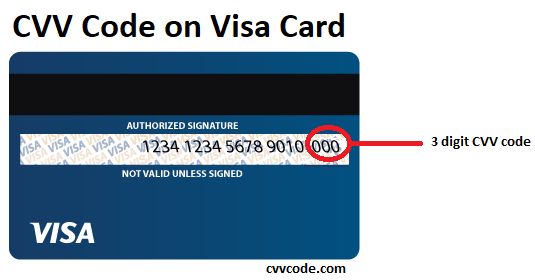

Card Verification Value Check (CVV)

This tool verifies the Card Verification Value (CVV) number against the credit/debit card data submitted by the buyer. The CVV is a unique 3- or 4-digit security code that confirms an online buyer has possession of the credit or debit card when making the transaction.

It’s located on the backside of a card, next to the signature box. The CVV works in a manner similar to a PIN, which verifies a customer’s identity when card payments are used in card-present transactions.

Image source:

https://qph.cf2.quoracdn.net/main-qimg-ba4f3021e3b5a31a944f4740ca9b0ee7

If the CVV code provided doesn’t match the card number, the transaction is automatically declined—in the same way a card payment is declined in a physical retail store if a customer enters the incorrect pin.

To protect customers and prevent fraud, the Payment Card Industry (PCI) standards restrict merchants and payment processors from storing customers’ CVV codes.

IP address checks

This check confirms that the buyer’s current IP address corresponds to the address associated with the credit card. For instance, if the IP address indicates the customer is in Canada, but the credit card is registered to a United States address, the transaction will be flagged for review.

While it’s possible that the customer is traveling while making the online purchase, it’s also possible that the credit card has been stolen. Further checks will help determine the legitimacy of the transaction.

If, say, that credit card has been used for multiple online transactions within a very short time frame, the buyer is probably using a stolen credit card. Criminals often use stolen credit cards quickly before the cardholder reports the theft or loss.

But if the shipping information matches the credit card address on file with the issuing bank, it’s possible the translation is genuine.

Machine learning

Fraud-scrubbing software also uses artificial intelligence (AI) technology and data analytics to protect businesses from financial loss. This helps detect behavioral anomalies in a customer’s pattern, which might indicate fraud.

For example, a large order made on a credit card used for small purchases will be flagged for review as it’s possible the buyer is using a stolen credit card.

By default, fraud scrubbing is only performed on initial payments. Recurring payments are exempt since the buyer’s identity has already been confirmed.

Related Terms:

- Fraud Prevention

- PCI Compliance

3. PCI Compliance

Definition of PCI Compliance

Payment Card Industry (PCI) compliance refers to the act of following the technical and operational guidelines set by the PCI Security Standards Council.

The council is a global regulating body that has laid down a set of requirements, known as the Payment Card Industry Data Security Standards (PCI DSS), to prevent credit card fraud and safeguard sensitive cardholder data.

PCI SSC was created by five major card networks, including Visa, Mastercard, Discover, American Express, and JCB. Each of these card networks enforces PCI compliance.

PCI compliance is required for all organizations that accept, process, or store a full primary account number (PAN) that includes any of the following:

- Cardholder names

- Expiration dates

- Card Verification Values (CVVs)

Image source: https://www.canva.com/photos/MAEAzSLz_PA-credit-card-on-a-laptop-keyboard/

Online stores and merchant processors are some organizations that must be PCI-compliant.

Failure to comply with the PCI DSS can cost merchants penalties and fines of up to $100,000 every month.

Acquiring banks additionally consider non-compliant businesses as high-risk and charge higher transaction fees, and may withdraw card-accepting privileges.

Some payment processors also charge a non-PCI compliance fee between $4.99 and $19.9 to incentivize merchants to be PCI-compliant.

What are the benefits of PCI compliance?

- Builds customer trust: Since PCI DSS are global standards, customers are assured of the safety of their payment information. This will build brand loyalty and protect your reputation.

- Prevent data breaches: Adherence to PCI requirements makes it difficult for cybercriminals to penetrate your network. This protects your business from fines and potential lawsuits that arise from data breaches.

- Sets a security standard: PCI standards set a baseline for security measures that companies can use to develop their security program.

The following are the 12 key requirements for PCI compliance.

- Use and maintain a firewall configuration to prevent unauthorized access and protect private data.

- Use strong password protection systems and change generic passwords on point-of-sale (POS) systems, routers, or any other third-party products.

- Secure stored cardholder data by encrypting it and conducting regular scans to ensure all data is encrypted.

- Ensure all data transmitted over public networks is encrypted.

- Install and regularly update antivirus software on all workstations that handle cardholder data.

- Use properly updated systems and applications, such as firewalls, antivirus programs, and POS terminals, to fix any existing security vulnerabilities.

- Restrict access to cardholder data to a “need to know” basis. This includes employees, managers, and third parties who should not have access to this information.

- Assign unique IDs to authorized users accessing cardholder data to increase accountability and improve response time in the event of a data breach.

- Sensitive payment information that’s kept physically, either written or typed, must be in a secured location with restricted access.

- Monitor and track all access to cardholder data by creating and maintaining logs of access.

- Conduct regular security systems and process tests to identify potential vulnerabilities and malfunctions that exist.

- Document policies and procedures for all systems, software, equipment, and authorized users’ access logs related to PCI DSS.

Example of PCI compliance in a sentence:

Maintaining PCI compliance must be a top priority for businesses to ensure the security of their customers’ payment information.

Synonyms: PCI DSS compliance

Related terms:

4. Tokenization

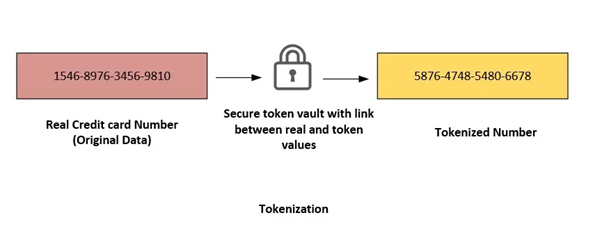

Definition of Tokenization

The process of replacing sensitive data with a non-sensitive surrogate value, known as a token. The token is made up of randomly generated characters that do not have any value or meaning.

The characters, however, have unique identification symbols that help identify the original data they represent. Tokens act as links to the token vault, where the actual sensitive information is stored.

Merchant processors use tokenization to protect sensitive data such as:

- Credit card numbers

- Cardholder names

- Bank account information

- Card Verification Value (CVV) codes

- Expiration dates

This helps them store the data securely and simplifies the payment process for returning customers, subscription payments, and recurring billing.

How does tokenization work?

Image source: https://www.encryptionconsulting.com/education-center/encryption-vs-tokenization/

The following is a sample transaction showing how tokenization works during a credit card payment.

- When John Smith (a customer) enters his payment information on an online checkout platform or a POS terminal, a payment gateway generates a token for the data. Instead of John Smith, account number 1235 6563 7464 6479, expiration date 12/27, the token 74uf*bsg1lsp%t8j is generated and used.

- The payment gateway encrypts the token and sends it to the payment processor. The actual payment information is stored in a secure token vault, which is the only component that matches a token to its underlying data.

- The processor encrypts the data again before sending it to the card networks for authentication.

- If the payment is confirmed, an after-payment confirmation is sent to all the relevant parties: the payment processor, the payment gateway, the merchant, and the customer.

How is Tokenization Different From Encryption?

Though tokenization and encryption are often used interchangeably, they are not the same.

Tokenization substitutes sensitive, private data with a scrambled data string, while encryption converts the original information into a secret code that hides its true meaning.

An encrypted code is generated mathematically and can be decrypted to reveal the hidden information. It’s, however, impossible to reverse a token since it’s randomly generated and has no relation to the information it represents.

The following table compares tokenization to encryption.

| Tokenization | Encryption |

| Token is generated randomly | Code is generated mathematically |

| Original information is stored in a token vault | Original information is hidden behind the encrypted code |

| Irreversible | Reversible |

| Used on structured data like credit card or bank account numbers | Used on both structured and unstructured data such as emails and entire files |

Both tokenization and encryption are used by merchants to ensure PCI compliance.

Businesses should use tokenization because it:

- Reduces their obligations under the Payment Card Industry Data Security Standards (PCI DSS) as they won’t be storing the actual payment details

- Ensures cardholder data privacy and security in the event of data breaches

- Speeds up transaction process since tokens allow for automation

Example of tokenization in a sentence:

Tokenization adds an extra layer of protection for store owners, which boosts customers’ trust.

Related Terms:

5. Transport Layer Security (TLS)

Transport Layer Security (TLS) is a security protocol used to secure an internet connection and protect sensitive information shared over the web. TLS is especially important for systems that exchange private data, as it ensures eavesdroppers can’t view the information.

Since payment processing involves the exchange of cardholder information across various parties, TLS is mandatory. In fact, the PCI security standards mandate the use of TLS to secure the transmission of payment information.

The TLS security protocol provides internet security through the use of certificates. Certificates are issued by a trusted certificate authority (CA) and are used to authenticate sites and encrypt and decrypt information shared between systems.

A website secured using TLS displays a locked padlock icon next to its URL.

Image source: https://medium.com/analytics-vidhya/process-of-classifying-malicious-and-benign-websites-815cc2b42435

How does TLS work in payment processing?

TLS certificates use authentication and encryption to secure sensitive payment information, such as:

- Primary Account Numbers (PAN)

- Card Verification Values (CVV)

- Service codes

Authentication verifies a TLS certificate is issued by a reputable CA and matches the domain name of the payment server. This prevents man-in-the-middle (MITM) attacks, where hackers intercept communication by posing as the payment server.

In contrast, encryption is the process of scrambling data using a mathematical algorithm, making it unreadable to unauthorized parties. The longer the encrypted data, the more secure it is since it’s harder to decrypt a long key than a short key.

The length of encryption is measured in bits, and the three most commonly used bit lengths are:

- 128

- 192

- 256

256-bit encryption offers the highest level of security since it’s nearly impossible to crack; it would take billions of years even for the most advanced computers to decrypt a 256-bit encryption code.

This makes it the most suitable encryption method for highly sensitive information, such as cardholder data.

A TLS certificate has two keys: a public key that encrypts data and a private key that decrypts it. When a customer enters their payment information on a checkout platform, the certificate on the host server encrypts the information and sends it to the payment processor.

The payment processor’s TLS certificate holds the only private key that can decrypt the information. This protects your business and customers from the financial damage that can result from data breaches.

Does your e-commerce website need TLS certification?

Yes, a TLS certificate is necessary for securing customer data and PCI compliance. You should also ensure that your payment processor uses TLS to secure data transmission and storage.

TLS certificates additionally offer the following benefits:

- Build customer trust: Securing your website using TLS assures your customers that you take their privacy and security seriously, which boosts trust, loyalty, and conversion rates.

- Improved fraud detection: The TLS protocol of authentication and encryption provides additional security features to help merchants prevent fraud.

- Improved user experience: Secure transactions powered by TLS reduce the risk of payment errors or transaction timeouts, improving the user experience.

Total Apps uses a combination of TLS 1.2+ and 256-bit encryption, providing a high level of security for all your transactions.

Related Terms:

Payment Processing

1. Card Network

An organization that provides payment infrastructure, enabling the processing of card transactions. The network regulates who, where, and how cards are used, as well as the fees that merchants pay for card transactions. Merchants or business owners do not have direct access to these organizations to set up accounts with them directly. They must go through a payment processor.

The five major card networks in the United States are:

- American Express

- Discover

- Mastercard

- Visa

- JCB

What is the role of card networks in payment processing?

Card networks authorize transactions and facilitate the transfer of funds by communicating with the payment gateway, the issuing bank, and the acquiring bank.

The issuing bank is the bank that lends unsecured credit to customers or houses the payee’s account in the case of a debit card. The acquiring bank, on the other hand, is the bank that receives the payments on behalf of the merchant.

When a customer makes a purchase, the card networks confirm with the issuing bank that the card has funds. They also verify that the payment won’t exceed the credit limit or bank account balance, if it’s a debit card.

Some other roles of card networks include:

- Setting interchange fees: Card networks set and review interchange fees, which are the charges paid to banks to compensate them for facilitating card payments. These fees are later passed on to merchants and make up a significant portion of transaction fees.

- Enforcing PCI compliance: The five major card networks in the US ensure adherence to PCI standards, which aim to reduce payment fraud and data breaches. They assess and enforce penalties for non-compliance, which may include fines or the termination of a merchant’s privileges.

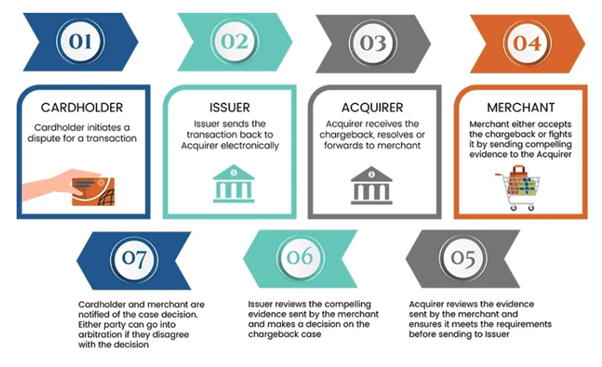

- Resolving chargeback disputes: Card networks make the final decision on whether a chargeback is issued or denied. They facilitate dispute resolution by arranging negotiations between the cardholder and the merchant.

- Provide fraud protection services: Besides enforcing PCI security standards, card networks also offer fraud prevention tools to verify customer identities. Some tools include 3-D secure authentication, Card Verification Value (CVV) codes, and chip cards.

The following is a sample transaction that demonstrates how card networks work.

- A customer makes a purchase using a Visa credit card at a grocery store.

- The grocery store’s point of sale (POS) terminal sends a request for authorization to the merchant’s processor, who acts as an intermediary between the merchant and Visa.

- The merchant’s processor forwards the authorization request to Visa, who then transmits the request to ABCD bank, the issuing bank.

- ABCD bank verifies the payee has sufficient credit and responds with an authorization code, which they send to Visa.

- Visa sends the authorization code to the payment processor, who forwards it to the grocery store’s POS terminal, indicating that the transaction is approved.

- The merchant completes the transaction, and the acquiring bank submits a request for payment to the card network.

- Visa routes the request for payment to ABCD bank, which transfers the funds to the acquiring bank.

- The acquiring bank deposits the funds into the merchant’s account.

Synonyms: Card associations, card schemes, payment networks

Related Terms:

2. Card-Not-Present (CNP) Transaction

Definition of Card-Not-Present Transaction

A payment that takes place when neither the cardholder nor the credit card is physically present. Customers initiate the transactions remotely through phone, email, or online.

Examples of CNP transactions include:

- Mail Order/Telephone Order (MOTO): A customer provides payment information over a phone call, traditional mail, or through email.

- Online purchases: Customers make payments for goods or services over the internet on the merchant’s website or marketplace.

- Recurring payments: Subscription payments, such as gym memberships, are automatically deducted from a credit card using the payment information stored by the merchant.

Services offered by payment processors, such as virtual terminals and payment gateways, enable CNP transactions.

Sometimes, as in recurring payments, the first payment may be a card-present transaction, but all subsequent payments are CNP transactions.

It’s also worth mentioning that some card-present transactions can also be processed as CNP transactions.

For example, if a customer service agent at a physical retail store manually entered credit card information on a virtual terminal, the transaction is considered a CNP transaction. The sales agent didn’t physically swipe or tap the credit card but submitted payment details online.

What is the difference between a card-present and a CNP transaction?

Card-present transactions occur when the credit or debit card is physically present and is tapped, inserted, or swiped using a credit card reader.

In contrast, CNP transactions occur when payment details are submitted online via a virtual terminal or on an online checkout platform.

The table below outlines more differences between card-present and CNP transactions.

| Card Present Transactions | Card-Not-Present Transactions |

| Require hardware tools, such as a credit card reader | Requires software tools, such as payment gateways and virtual terminals |

| Secure and have a lower risk of fraud | Run a higher risk of fraud |

| Low transaction fees | Higher transaction fees than card present transactions |

Some advantages of accepting CNP transactions include:

- Improved sales: It’s more convenient for customers to make payments remotely than physically, which boosts sales.

- Simplified payments: CNP transactions enable recurring billing, saving businesses time and effort spent in collecting payments.

The downside of CNP transactions is that they are associated with a higher risk of fraud and chargebacks, which increases the processing fees.

Verifying the buyer’s identity is difficult in CNP transactions, which makes them an easy target for fraudsters using stolen credit cards. In fact, 80% of all fraud incidents reported in the US in 2021 were from CNP transactions.

Due to the higher risk, card networks and banks charge higher transaction fees. For instance, the average Visa interchange rate for card-present transactions is 2.10% + $0.10, while CNP transactions are charged at 2.89% + $0.25.

To mitigate these risks, payment processors use fraud scrubbing tools such as the Address Verification Service (AVS) to detect and prevent fraudulent activity.

AVS confirms the billing address provided by the customer with the billing information on file at the issuing bank or credit card network. This helps mitigate fraud from stolen credit cards.

- Payment gateway integration: Adding any of Total Apps’ gateways to your checkout platform allows your firm to accept CNP transactions.

- Virtual terminal: Total Apps offers virtual terminal services to enable firms to process payments from customers who make orders in any form such as over a phone call or in person.

Related Terms:

3. Merchant Account

Definition of Merchant Account

A specialized bank account that allows businesses to accept electronic payments from their customers.

The bank account holds funds from customers’ payments for 1–2 days before the money is transferred into a business bank account.

Think of it as a cash register in a traditional brick-and-mortar store that holds cash payments before someone deposits the money into a business bank account.

Online and physical retail stores need a merchant account to accept electronic payments.

A merchant account protects the store owners from the uncertainties associated with online payments. For instance, if a customer requests a chargeback, the funds are available for return since they’re temporarily held in the merchant account.

How is a merchant account different from a business bank account?

Merchant accounts process credit or debit card payments faster than business accounts.

If a payment is made directly to a business account, the transaction will remain pending until both the issuing bank and the merchant’s bank authorize it. This takes up to five days and hurts cash flow.

A merchant account, however, receives the money immediately, even if the transaction is pending. Payment processors, who provide merchant accounts, take on the risks that come with electronic payments, enabling businesses to receive payments faster.

The table below compares a merchant account and a business account.

| Merchant Account | Business Account |

| Manages electronic payments only | Manages all business funds, including cash and checks payments |

| Doesn’t allow cash or check deposits | Allows cash and check deposits |

| Merchants have no control over the account and can’t make withdrawals | Merchants have full control over the account and makes withdrawals and payments from the account |

How to get a merchant account

A merchant account is provided by a merchant processor or an acquiring bank.

Merchant processors make agreements with the acquiring bank (the bank that receives the customers’ payments) and act as intermediaries between merchants, the issuing bank, and the acquiring bank.

You can apply for a merchant account with a payment processor, who’ll vet your application by reviewing business information such as your:

- Credit history

- Type of business

- Estimated transaction volume

- Time active in business

As a merchant account is a type of business account, you’ll also need to provide statutory information, such as:

- Legal business name and address

- Business license number

- Tax ID number

The merchant provider will approve the application after vetting it, and you can begin receiving online payments.

Synonyms: Credit card processing account

Related terms:

- Merchant Processor

- Setup Fee

- Transaction Fee

4. Merchant Processor for Payment Processing

Definition of Merchant Processor

A financial service company that executes transactions on behalf of the merchant. The processor ensures proper funds are transferred from the payee’s account to the merchant’s account.

The company supports its function by providing the essential equipment the merchant requires to accept electronic payments. The equipment can be in the form of hardware tools like a credit card reader or software application, like a payment gateway.

For instance, for card-not-present (CNP) transactions, a merchant processor will provide a payment gateway to enable communication from the checkout software to the issuing bank.

Image source: https://www.hippopx.com/en/credit-card-payment-credit-card-money-business-shopping-94862

The role of a merchant processor is similar to that of a cashier in a physical retail store. When a customer makes a cash payment, the teller takes the money from them, confirms it’s the right amount, and then deposits it in the cash register.

A merchant processor works in a manner similar to the cashier. The company facilitates the transfer of proper funds from the payee’s account (customer’s hand) to the merchant’s account (cash register).

The processor also deducts interchange, transaction fees and any other fee from the customers’ payments before depositing the gross payment in the merchant’s account.

So, how is a merchant processor different from a payment gateway?

A payment processor is an entity that enables the processing of payments, while a payment gateway is the software application that allows communication from the checkout software to the issuing bank.

The table below shows more differences between a payment processor and a payment gateway.

| Payment Processor | Payment Gateway |

| Company that works as a middleman between the issuing bank and the merchant’s account | Software service that connects the payment software to the issuing bank |

| Provides equipment to enable the merchant to accept card payments | Is one of the software tools provided by the payment processor to enable a merchant to accept online payments |

| Necessary for both card present and CNP transactions | Widely used for CNP transactions |

A payment processor helps business owners streamline their operations, thus increasing their profitability. Without one, business owners would have to process all transactions manually, which is time-consuming and tedious.

Payment processors also offer a wide range of features that businesses benefit from, such as:

- Fraud prevention

- Mobile payments support

- Data analytics tools and reporting

- Branded invoicing and receipts for each customer’s use

- Foreign Currency Exchange

- Account Updater

Here are some factors to consider while choosing a merchant processor.

- Multichannel payment methods: The ideal payment processor should offer your customers multiple ways to pay, such as credit or debit cards, digital wallets (Apple Pay or Google Pay), ACH, or bank transfers. This will improve sales since customers are more likely to complete purchases with multiple payment options.

- Compatibility with all devices: Potential customers will browse and shop for products on your website from different devices. A payment processor that’s compatible with multiple devices, such as mobile phones and tablets, will increase your sales revenue since customers can complete impulse purchases instantly.

- Simplicity: It’s important to choose a merchant processing platform that’s simple and easy to use. A user-friendly platform will make the checkout experience pleasant for your customers.

- Security: To safeguard your customer’s payment information, ensure the merchant processor is compliant with PCI security standards. The processor should also implement fraud prevention measures, among other screening technologies.

- Fees: Consider the charges associated with the merchant processing services, such as the setup fees, transaction fees, and monthly fees. Conduct research and ensure your service provider is not overcharging you, thus reducing your profit margin.

- Customer service support: Choose a payment processor that offers 24-hour customer service support. In case anything goes wrong, the service provider will provide technical assistance and help fix the problem so you don’t lose sales.

“ … had a problem processing a payment and before I could get it resolved myself, Total Appscustomer support proposed a resolution. If you want a processor who has your back, choose Total Apps.” – Kevin Crump, CEO Magnavon Industries, CEO, QuantRM.

Synonyms: Credit card processor, payment processor, payment service provider Merchant services provider

Related terms:

- Payment Gateway

- Payment Gateway Integration

5. Payment Gateway

Definition of Payment Gateway

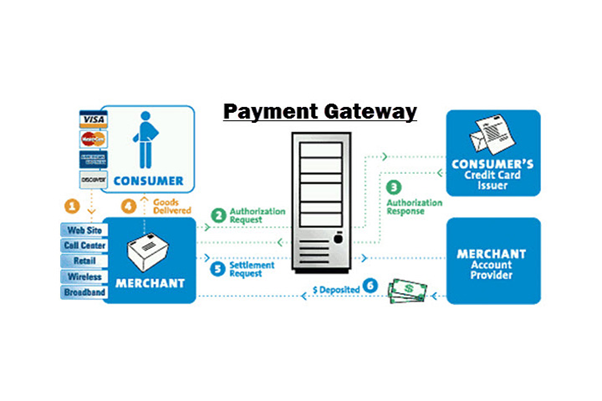

A secure network through which merchants accept payments from their customers. It’s the connection between the checkout software and the bank that will authorize the credit card payment.

Its role is to securely transmit sensitive payment information from the point-of-sale (POS) or checkout software to the issuing bank.

Simply put, a payment gateway is a digital connection between the merchant and the issuing bank.

How does a payment gateway work?

Image source:

http://i-verve.com/blog/payment-gateway-integration-ecommerce-website-stores

When a customer comes to your website’s payment page to make a purchase, they’ll enter their card details to complete the purchase.

A payment gateway captures and encrypts the data, then sends it to the processing bank.

The processing bank will confirm that the customer has adequate funds to make the purchase. If they do, the payment gateway will relay to the customer that the transaction has been approved.

In the case a transaction exceeds the account balance, the payment gateway will similarly relay to the client that the transaction has been declined.

The store owner is not involved in this process and only fulfills the order when the transaction is complete.

Though payment gateways are prevalent among online stores, physical retail stores also use them to process electronic payments. The software service is used online or through a POS.

Let’s take an example of a physical retail store that takes orders over the phone.

When a sales representative takes an order, he or she will manually enter the payment information online via a virtual terminal.

The payment gateway completes the transaction cycle by communicating with the issuing bank and then relays the approval or denial of the transaction to the sales representative.

Businesses that can benefit from a payment gateway include:

- eCommerce stores

- Non-profits

- Service companies

Why does your business need a payment gateway?

- Fast payment: Your customers don’t have to wait to make a purchase as payment gateways ensure instant card or bank payments.

- Easier payment of invoices: Service providers, such as plumbers or electricians, who regularly send out branded invoices can enjoy a more seamless invoicing experience and get paid through a payment gateway faster.

- Convenience: With payment gateways, your customers can make purchases at any time—day or night, and even when you’re not minding your online store. This allows you to focus on other areas of your business.

- Secure transactions: Payment gateways must comply with Payment Card Industry Data Security Standard (PCI DSS) requirements, which ensure the security of customers’ data and payment information. This also reduces credit card fraud, as only the issuing bank has access to the customers’ information.

- Improved user experience: Returning customers don’t have to input their payment information with every purchase. The checkout process is simplified since they use the stored payment information and checkout with just a few clicks.

Example of payment gateway in a sentence:

Total Apps is a payment service provider with a built-in payment gateway that enables safe and efficient processing of funds to merchants’ accounts. Total Apps is gateway agnostic and is able to use any gateway a customer chooses.

Synonyms: Merchant gateway, pay gate, online gateway

Related terms:

- Merchant Processor

- Payment Gateway Integration

6. Payment Gateway Integration

Definition of Payment Gateway Integration

The process of adding a payment gateway to an eCommerce website, app, or point-of-sale (POS) system. Integrating a payment gateway allows customers to make instant and secure online payments on a website or POS system.

Some payment processors also allow payment gateway integration with other software systems, such as customer relationship management (CRM) and accounting software.

With your software systems integrated, your employees don’t have to re-enter data on another system after each sale. This creates harmony, promotes the smooth flow of information, and saves your business valuable time.

To ensure this, look for a payment gateway integrated with an application programming interface (API), which will allow you to seamlessly add all your software systems.

Some other benefits of integrating a payment gateway include:

- Lower labor costs: When your payments are automatically added to the general ledger, an accountant doesn’t have to go over the purchases and reconcile the accounts. It’ll additionally take less time for your staff to use the payment integration tools.

- Accurate bookkeeping: Instances of overcharged customers or duplicate data will be a thing of the past with integrated systems. You’re confident that the data collected is an accurate representation of your business and that customers are also billed properly.

- Improved cash flow: An integrated payment system provides current and reliable reports on how much is available in your business account, at the end of the day. This will help you manage inventory, pay suppliers, and make better operating decisions.

Image source: https://dribbble.com/shots/5713615–002-Credit-Card-Checkout

There are two main payment gateway integration methods, as detailed below.

API-hosted integration method (Onsite Payments)

This method allows eCommerce sites to process payments using an application programming interface (API). There’s no redirection involved, as the API enables communication between the checkout platform and the payment gateway.

The API-hosted integration method offers merchants fully customizable interfaces and integration with multiple devices, such as mobile phones, tablets, and computers.

Merchants have more control over the checkout experience and can customize the payment page to match their website. They are, however, responsible for the security of payment information and must ensure PCI compliance for their websites.

Hosted payment gateway integration (Offsite payments)

In this method, the merchant processor hosts the payment page. The customer has to leave the merchant’s website and is redirected to the service provider’s page to complete the payment.

Hosted payment gateways are customizable and include your store’s name and branding. They are typically used by merchants who don’t have a secure site.

Once the customer completes the purchase, they’re redirected to your website to finish the checkout process.

Unfortunately, redirection to another page can cause the customer to think they are being duped into giving away their credit card information. There’s also a slight delay in redirection which negatively impacts the customers payment experience.

This can cost you sales since customers will probably abandon the purchase when they can’t trust your site or when the process takes too long.

The table below shows the pros and cons of each of these payment integration methods.

| Payment Integration Method | Pros | Cons |

| Hosted integration | ● Customizable payment page

● Merchants’ website doesn’t require PCI compliance |

● Merchant has no control of the checkout experience

● In the event of a network error, customers might not be redirected to your website after a payment |

| API integration | ● Easy to set up

● Safeguards sensitive customer data ● Full control over the users’ payment journey ● Compatible with multiple devices |

● Merchants’ website needs to be PCI-compliant

● Merchants have to maintain the infrastructure on the payment page interface |

Synonyms: Payment integration, payment processor integration

Related terms:

7. Virtual Terminal for Payment Processing

Definition of Virtual Terminal

A dashboard on a payment gateway that allows merchants to accept card payments in card-not-present transactions. Call center agent, sales representatives, or customers manually enter the payment details.

It’s referred to as a “virtual terminal” since it’s hosted online as opposed to a physical terminal like a credit card reader.

Virtual terminals allow businesses to accept payments from customers without requiring their physical presence. They’re provided by merchant processors and integrated with payment gateways to allow for quick payment processing.

All businesses that take orders or payments remotely (either by phone or email) need a virtual terminal. Some of them include:

- Restaurants

- Freelancers

- Service-based businesses, such as tax accountants or lawyers

How do virtual terminals work?

Virtual terminals work in a similar manner to physical terminals, but are instead hosted online.

Here’s how a sample transaction on a virtual terminal works.

- The merchant’s staff opens the virtual terminal by logging in to the payment gateway.

- Employees manually key in the payment details, such as the credit card number, the expiration date, and the billing address, on the payment gateway’s dashboard. Staff can do this while still on the phone with the customer.

- The sales agent submits the transaction details.

- An after-payment confirmation or rejection is sent back to the virtual terminal.

- The sales representative confirms with the customer whether the payment was confirmed or declined.

Benefits of using virtual terminals

- Easy to set up and use: A virtual terminal requires no hardware tools—merchants only need an internet connection.

- Faster payments: It only takes a few minutes to process payments on a virtual terminal, as opposed to waiting for the client to send in a check or money order, which takes days.

- Secure transactions: Merchant processors use techniques such as end-to-end encryption and tokenization to ensure the security of the payment information transferred over public networks.

- Allows recurring billing: Virtual terminals enable businesses to set up recurring payments. This saves time since the merchant doesn’t need to track down the customer every month for their payment.

Disadvantages of using virtual terminals

- Virtual terminals are time-consuming compared to physical terminals since the merchant’s agent has to submit the cardholder data manually.

- Like all card-not-present transactions, virtual terminals also carry a higher risk of fraud. Customers can call and use stolen credit cards since there’s no way to verify if they’re the card owners.

Merchant processors, however, mitigate the risks of fraud by using fraud prevention and detection tools. Total Apps for instance, uses fraud-scrubbing tools such as the Address Verification Service (AVS) and Card Verification Value (CVV) to prevent and detect fraudulent transactions.

Related Terms:

8.Chargeback

Definition of Chargeback

A reversal of funds to a customer after the buyer successfully disputes a credit or debit card transaction. The chargeback process is initiated by the cardholder with the issuing bank and applied if the customer can’t provide sufficient proof of the situation at hand why they are charging back and not getting a refund directly from the merchant owner.

Image source: https://hoteltechreport.com/news/chargeback

Chargebacks protect customers from financial crime and unscrupulous businesses that sell subpar products and/or services.

They, however, cause revenue loss to genuine merchants who pay expensive chargeback fees and lose sales revenue. The merchants themselves might also be victims of fraud perpetrated by fraudsters or dishonest customers.

There are four main types of chargebacks, as detailed below.

- Clean fraud: A fraudulent transaction that appears legitimate goes through, but the cardholder disputes the payment. This might be the case when fraudsters use stolen credit cards to make online purchases.

- Merchant error: The merchant makes a mistake and fails to deliver the product or ships the wrong item.

- Chargeback fraud: When a dishonest customer initiates a chargeback, claiming that they never received the products or services paid for. In this case, the customer is trying to defraud the merchant by asking for a refund for products or services they rightfully received.

- Friendly fraud: A cardholder disputes a legitimate transaction, thinking they might be a victim of fraud. This occurs when a customer makes an honest mistake, like in a case where a cardholder simply forgets about the purchase.

Chargebacks are different from refunds, which are return payments voluntarily made by merchants without intervention from the issuing banks. Businesses offer refunds to appease dissatisfied customers and improve brand loyalty.

The table below lists the differences between chargebacks and refunds within five distinct areas.

| Chargebacks | Refunds | |

| Communication | Customer bypasses the merchant and disputes the transaction with the issuing bank | Customers and merchants work together to find a solution beneficial to both parties |

| Clarity | Merchants make assumptions on the cause of the chargeback | Customers explain the underlying issue to the merchant |

| Fees | Banks charge high transaction fees for processing chargebacks | No fees are associated with refunds |

| Returns | Merchants don’t get their products back since they aren’t communicating with the customers directly | Merchants can negotiate for the return of the products purchased |

| Time | Are time-consuming and take months to resolve | Are easy to resolve and can be completed within one week |

Chargebacks are subject to processing fees charged by the acquiring bank, which can result in massive losses and bankruptcy. These fees range between $20–$100, on every transaction, depending on the acquiring bank.

There’s also an additional transaction fee between $0.10 and $0.30 charged on every chargeback processed.

In addition, banks can deny merchants with excessive chargebacks the right to process card payments.

The best way to avoid such consequences is to implement measures that help prevent and reduce chargebacks, such as:

- Complying with Payment Card Industry (PCI) regulations: PCI compliance helps prevent and detect fraudulent transactions that might ultimately result in clean fraud chargebacks.

- Using fraud-scrubbing software: Ensure your payment processor uses fraud-scrubbing techniques to protect your business from clean fraud chargebacks.

- Tracking shipped orders: This will provide documentation and proof of delivery, which will reduce chargeback and friendly fraud incidents.

- Offering impeccable customer service: Some customers may initiate chargebacks due to frustrations with your customer service. Ensure your customer service agents promptly respond to customer’s complaints and provide timely solutions.

- Providing clear product descriptions: Make sure every product on your online store has a clear description of its size, weight, and make. This will help create accurate mental images and prevent chargebacks from dissatisfied customers.

Working with a payment processor who offers chargeback management services will help you effectively manage reversal disputes. It’ll shift the problem to your merchant processor, allowing you to focus on growing the business.

Synonyms: Reversal, Payment dispute

Related terms:

9. Recurring Billing for Payment Processing

Definition of Recurring Billing

A payment model that enables businesses to automatically charge their clients for goods or services provided on a regular billing schedule.

The schedule can be weekly, monthly, or quarterly, depending on the arrangement the business has with its customers.

Recurring payments are card-not-present (CNP) transactions that are set up either by the customer or a sales agent via a payment gateway. As such, merchants need a payment processor to accept and set up recurring billing.

Customers only need to provide their payment information once, during the initial sign up. All subsequent payments are automatically charged on the credit or debit card provided.

Recurring billing is often used by subscription-based businesses, such as:

- Wellness industry firms with supplement or diet pills

- Digital entertainment companies, such as Netflix

- Online learning platforms

Some other businesses that use recurring billing include:

- Service-based businesses that collect regular payments such as utility companies

- Membership-based businesses, such as clubs and gyms

- Business that offer payment plans, such as lawyers, who often break down large payments into smaller, regular scheduled payment

There are two types of recurring billing.

Fixed payments

The merchant bills the customer the same payment amount every transaction cycle. For example, gym memberships charge fixed recurring payments—the customer pays the same amount, say $50, every month.

Irregular payments

The customer pays a varying amount on every payment cycle, depending on the usage of the product or service. For instance, the amount paid for an electricity bill will vary every month depending on the usage.

Is subscription billing similar to recurring billing?

Recurring billing and subscription billing are often used interchangeably since they have many similarities, including:

- Payment information for payment processing is provided at the time of signup

- Charges are deducted automatically on a regular schedule

The two, however, have one difference.

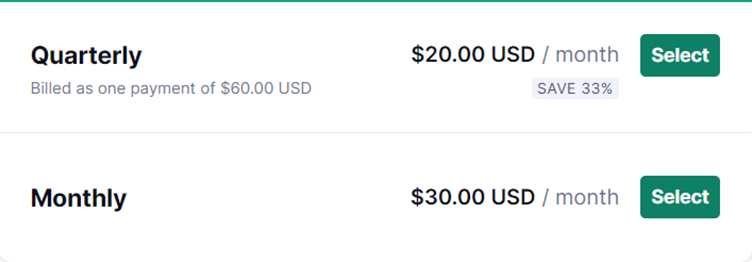

Subscription billing has many pricing plans for customers to choose from. Customers can pay higher or lower fees depending on the pricing plan they choose. Recurring billing, however, has no pricing tiers.

The following is a sample subscription billing plan with two pricing tiers from an online writing assistant.

Image source:

https://www.grammarly.com/upgrade?utm_campaign=kazaSubscription&utm_medium=internal&state=ekPsjhQpzlvPAlg&utm_source=kaza

Some benefits of using recurring billing are:

- Improves customer retention: Customers will be more loyal to your business because of the convenience that comes with recurring payments.

- Better cash flow management: Businesses make smart operating decisions because they already have a projection of the sales revenue from recurring payments.

- Simplified payment processing: Recurring billing just needs one quick sign up. Subsequent payments are charged automatically, so businesses and customers have less work later.

- Lower billing costs: Payments are automatically charged, so merchants don’t have to track down their customers to bill and collect payments.

Unfortunately, recurring billing can result in an increase in chargebacks in the event of billing errors.

To prevent this, merchants should strengthen the customer service team to ensure reported errors are looked into and corrected immediately before subsequent payments are due.

Another way to reduce chargebacks is to keep your company’s information found in a credit card statement clear with your contact information so customers can cancel or renegotiate fees to stay easily.

Related Terms:

10. Split Payments in Payment Processing

Definition of Split Payments

A transaction method that allows the division of payments, using a specialized service.

Transactions processed through a payment gateway or point-of-sale (POS) terminal can be split into multiple portions payable using two or more payment methods or to multiple parties.

Split payments is a proprietary technology offered by select payment processors that merchants and customers use as follows.

How merchants use split payments for better payment processing

Businesses that connect buyers and sellers can split incoming funds between multiple vendors, deduct commissions, and deposit funds into their bank accounts.

The payments are split as fixed amounts or as percentages of the total transaction, depending on the merchant’s arrangement with the vendor.

For example, a marketplace may have an agreement with a seller that 3 percent of every sale is the merchant’s commission. If, say, a customer buys an item worth $100, the payment is split by percentage. $3, which is 3 percent of $100, will remain with the marketplace, while $97 (97 percent of the item) is sent to the vendor.

The following is a sample transaction showing how online marketplaces use split payments with multiple vendors:

- A customer makes a purchase of two products from sellers A and B.

- The buyer pays for the products in a single transaction remotely via a payment gateway.

- Funds from the customer are received by the online marketplace.

- A split payment is initiated based on the split information provided.

- Split funds are sent to seller A and seller B as per each vendor’s settlement cycle.

- The merchant’s split commission is deposited into the merchant account.

Split payments simplify the payment process for merchants—they don’t need to reconcile the accounts manually since the process is automated.

Some other contexts that merchants use split payments include:

- Merchants managing multiple business accounts: Daily deposits are automatically split and transferred to the various accounts.

- Platforms that offer on-demand services: Incoming customer payments will automatically pay vendors, service providers, and the company’s commission.

Businesses should use split payments for payment processing because they:

- Enable the faster processing of funds

- Allow merchants to pay suppliers and independent software vendors (ISVs) in real time using customers’ daily deposits

- Save labor costs since merchants don’t need accountants to manually reconcile accounts

How customers use split payments

With split payments, customers can settle a single transaction using multiple payment methods. A customer can use two different credit cards to pay for one item, or a group of people sharing a cab can split the bill among themselves.

Split payments are common in retail stores where customers complete transactions using cash and credit card payments. For example, a $100 purchase can be split with $50 paid in cash and $50 using a credit card.

Most online stores also allow customers to split payments between a gift or loyalty card and a credit or debit card. Here’s an example of a split payment in use for a card-not-present (CNP) transaction.

- A customer makes an order of $100 on an online store.

- Customer redeems loyalty points to pay for the order with the checkout platform.

- The customer’s loyalty points are equivalent to $20.

- To account for the gap, the buyer uses a credit card to settle the $80 deficit.

- A mixture of loyalty points worth $20 and $80 from a credit or debit card completes the transaction.

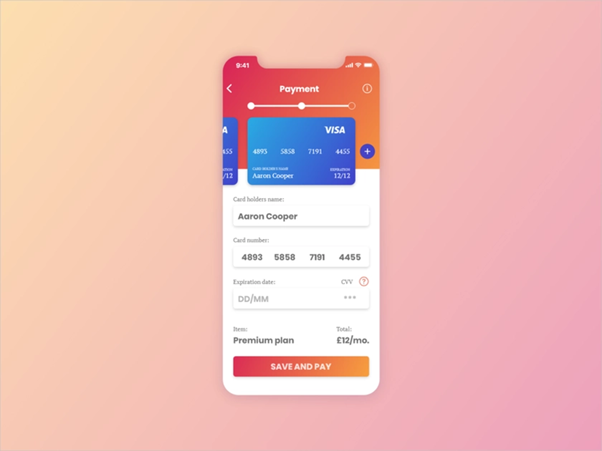

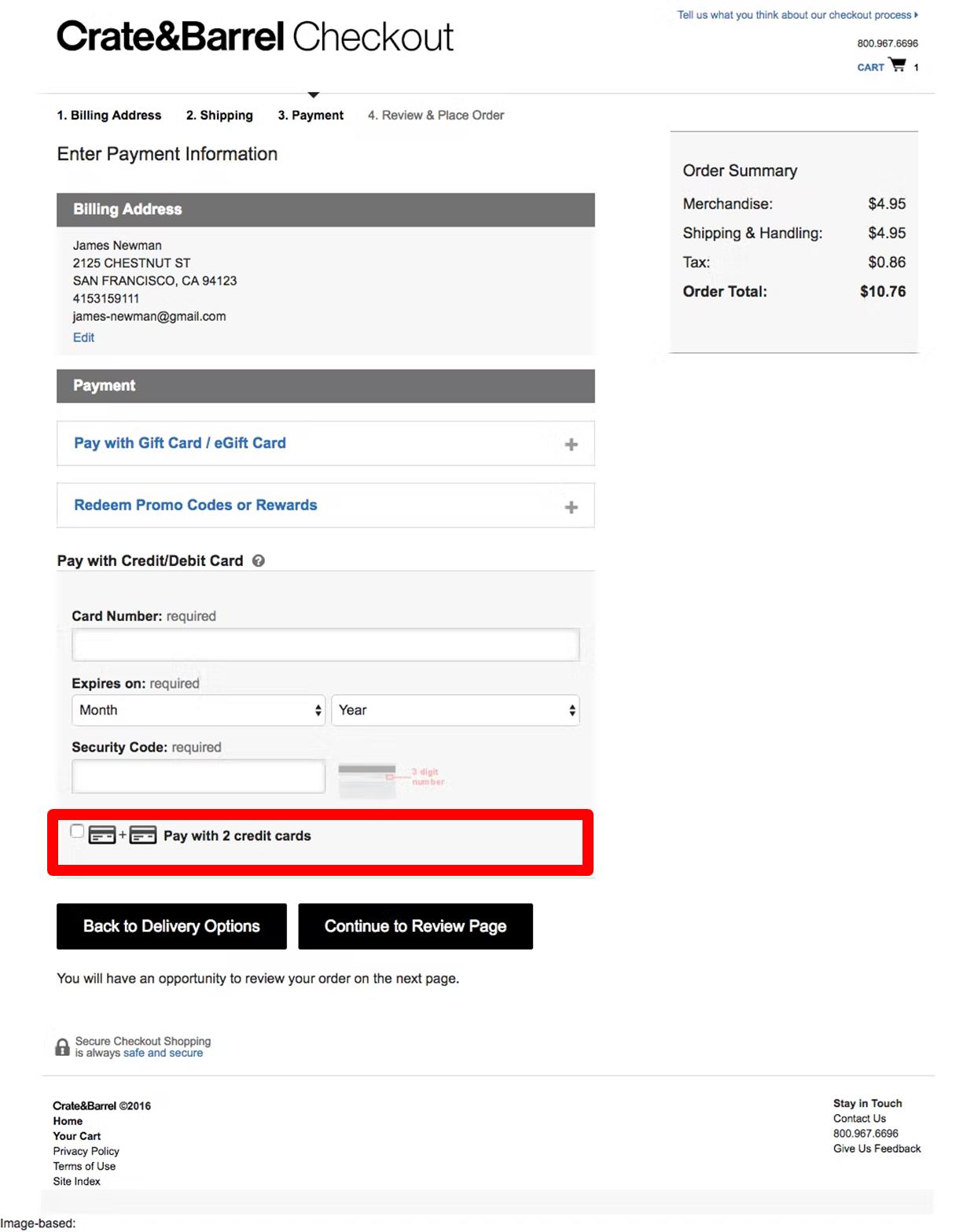

Very few online stores, however, accept split payments between two credit and/or debit cards. The process of verifying two cards in a single transaction is quite complex, but not impossible.

Image source: https://baymard.com/blog/perceived-security-of-payment-form

Both cards would need to be scrutinized by running fraud scrubbing checks to verify the legitimacy of the transaction, which requires pretty sophisticated technology.

Multiple card payments also complicate the chargeback or refund process and present a big window for fraudsters to exploit.

Split transactions, however, give customers more convenience to complete purchases, which improves sales since customers find it easier to pay for their orders.

Synonyms: Split transactions

Related Terms: